Check out our Top Rewards Cards to boost your points earning and travel more!

Amex has been pummeled in the high-end market with the introduction of the Chase Sapphire Reserve and in the everyday market with the loss of their Costco relationship.

Disclaimer: I am not a credit card marketing affiliate. All links in this post are for reference only. I will not be compensated for your use of any links in this post.

Chase Sapphire Reserve is Simple

The marketing genius of the CSR is its simplicity. Head to head, the Amex Platinum has many more benefits than CSR. Yet in an app world where attention spans don’t reach the end of sentences, Amex makes complicated changes to the personal and business Amex Platinum cards.

I wonder how many CSR holders even know or care about airline and hotel transfer partners that those of us in the miles and points hobby prize so highly. Someone not obsessed with miles sees (1) 1.5 cents/point value when booking travel, (2) those instant travel credits popping up to the tune of $300/year, and (3) some airport lounge access. CSR is a Visa Infinite card that stripped out the headline Visa Infinite $100 Companion Airfare Discount and it didn’t matter.

Back in Amex land you add complicated Uber credits to complicated airline benefits. You add category bonuses that trigger only if you book through Amex. You add point rebates then within a half year slow down their processing and decrease the rate.

The EveryDay cards have a companion app to track your transactions each month to try to get the point bonuses you expect. Why should a card need an app just to aid customers in getting their points?

Surprise Launch of the Blue Business Plus Card

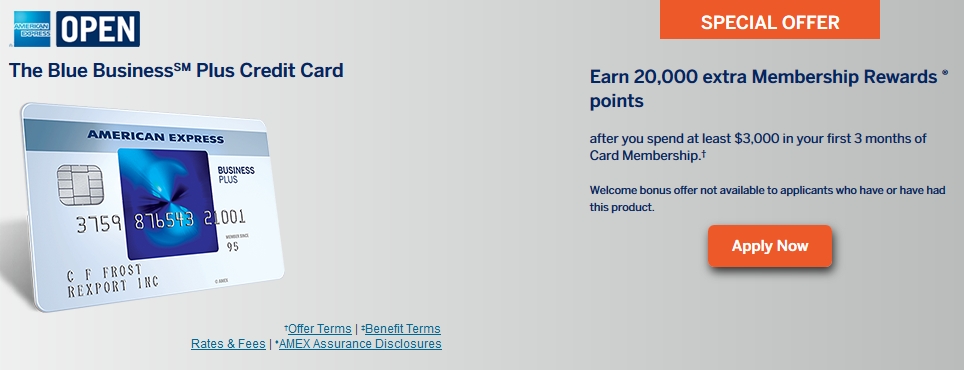

Today’s launch of the Blue Business Plus Credit Card is huge turnaround in Amex’s approach.

This is a no annual fee business card that earns 2 points per dollar everywhere up to $50,000/year. Spend over $50,000 earns 1 point per dollar. That’s it. No gimmicks, just swipe and earn.

The headline is that these are Membership Rewards points that can transfer to airlines and hotels. Unlike the personal Chase Freedom or business Chase Ink Cash, you do not need to pair the Blue Business Plus with an expensive annual fee card to transfer to travel partners. Now who’s simple?

If you want to get complicated, you can pair with other Amex cards, such as the Amex Business Platinum, to boost value. If you apply or upgrade to Amex Business Platinum by May 31, 2017, you will have a year of 50% points rebate on Pay With Points tickets in premium cabin on any airline, or in economy on the airline you choose for you annual travel credit. Existing cardholders are cut off on May 31, 2017 except those who applied for the card after from October 6, 2017, when the benefit was introduced.

The thing is, you don’t need to get fancy or pay high annual fees. Just get the Blue Business Plus and earn 2x points that can be used for cash or mile transfers. I finally have a card to recommend to my dentist who likes occasional leisure travel and doesn’t want to juggle cards.

Simple is Different than Beginner

If you are starting out in the miles and points hobby and are able and willing to get many credit cards, then going first for cards with big bonuses is the smart play.

A big sign-up bonus is a lot easier than trying to generate $50k spend on this card. This is a card for people either want it simple or who have exhausted other bonuses and can generate a high amount of spend.

Make Sure to Get a Sign-Up Bonus

The best launch offer is 20,000 points for $3,000 spend in your first 3 months of Card Membership.

The Amex website is not advertising a sign-up bonus.

Doctor of Credit has found this non-affiliate link with the offer.

All marketing affiliates have the bonus offer, and you’ve been hearing from them all day.

Keeping Points Alive

The Blue Business Plus joins the EveryDay card as a no annual fee method to keep Membership Rewards points alive. Say you have a big annual fee coming up or have a corporate card stash and are about to leave you job. Once you get this card and link your Membership Rewards accounts, all your points will be safe, even if you close the other cards.

Claw-Backs on the Horizon?

Amex yanking bank Membership Rewards points for 100k Platinum offers still hurts.

This is a Membership Rewards earning card so may be up for scrutiny.

Reasonable risk-reward approach is to use organic spend for first $3k to collect the bonus, then if you use methods such as gift cards to expand your spend volume, do that from $3k onward.

Short-Lived?

Other no annual 2% cards have come and gone. The Citi Double Cash is a current option that has had staying power. None have mile transfers.

Since this is a business card and Amex is capping 2x at $50,000/year, maybe the card will be sustainable. I’m not counting on that. I’ll be jumping in and maxing out this card as soon as I can.

I currently have 5 Amex credit cards in addition to my charge cards. I don’t expect them to soften the rules to allow 6, so only downside is giving up a current card I like.

Readers, will you be getting the Blue Business Plus Credit Card?

Related posts:

Check Out Our: Top Rewards Cards ¦ Newsletter ¦ Twitter ¦ Facebook ¦ Instagram

[…] is usually the other way around! Best post to read about the card is this one by Rapid Travel Chai: Out of the Blue: Amex Launches Awesome 2x No Annual Fee Business Card. You know it is a game changer when DansDeals calls it a “spectacular new card […]

Decisions, decisions, what will you give up?

I have Hilton for upgrade-downgrade offers, then Delta Platinum personal + business and Delta Gold personal + business. I got the Golds last fall since I had not had them before. Then they ran some nice refer-a-friend offers on all. I maxed them out for this year. My hesitation in giving them up is do I go to all the work to spend on this new card or sit on my Deltas and hope next year there are good refer-a-friend offers. I don’t easily generate huge amounts of spend. This dilemma is why I don’t have an EveryDay card, any… Read more »